Startups, Incubation, Acceleration. Are you Lost too ?

Facebook, Zynga, Foursquare have become house hold names today. There’s a certain excitement in running one’s own business, the charm of being an entrepreneur, the thrill of managing a team; but with every startup comes a set of hurdles and challenges.

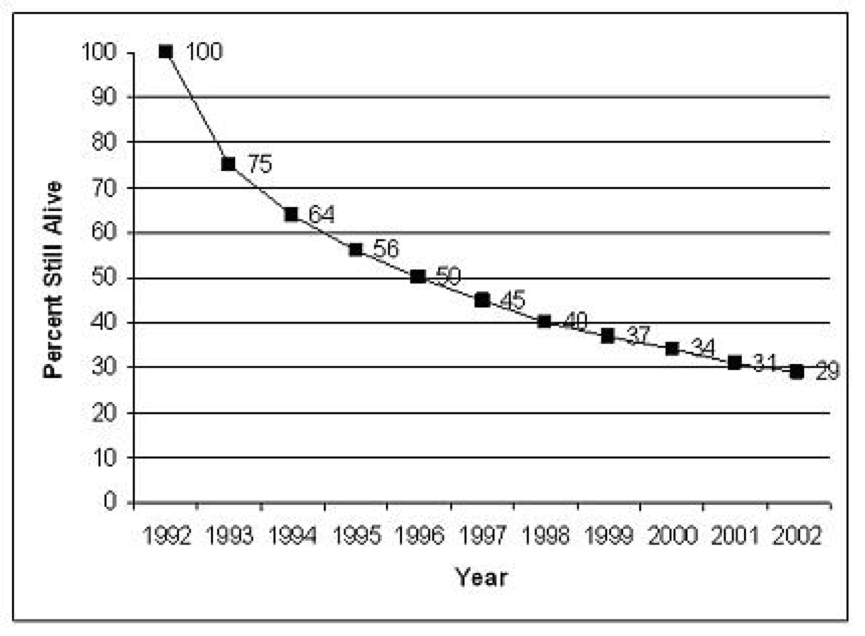

Before getting all thrilled about running a startup, it’s essential to understand the naked truth and prepare yourself to avoid the unforeseen. The graph below clearly shows the proportion of new businesses founded in 1992 still alive by 2002.

A study by Brian Headd and Bruce Kirchhoff found that only 28 percent of businesses with employees have any employment growth from one year to the next.

If you start a business, odds are that your company will fail. Data from the U.S. Small Business Administration shows that regardless of the year when they are founded, the majority of start-ups go out of business within five years, and two-thirds are no longer operating ten years after being formed.

So why do most startups fail?

To cut the chase, failure rates are high because a large number of inexperienced entrepreneurs start businesses that shouldn’t be founded in industries that are unfavorable to new companies. Most entrepreneurs pick unfavorable industries because low entry barriers attract them. Census data show that the rate at which entrepreneurs start businesses in different industries correlates 0.77 with the rate at which businesses fail in those industries. That is, entrepreneurs favor the very industries in which businesses are most likely to go under.

Interestingly, most entrepreneurs start companies that don’t even have a competitive edge. Data from the Panel Study of Entrepreneurial Dynamics reveals that this figure is nearly 40%.

Most entrepreneurs don’t have sufficient experience or exposure in the industries they are diving into. Research shows that working in an industry for several years before starting a business enhances the survival prospects of a start-up.

Other failure factors include lack of careful financial controls, marketing plans or even a basic business plan.

True, some start-ups fail because of factors beyond their founders’ control. But responsibility for much of the high failure rate of new businesses lies with the entrepreneurs themselves.

How does one overcome these challenges and how can one seek help?

Startup incubators are a brilliant way to stride through these challenges as the support that you get during the initial phases can make the difference between success and failure. These incubators provide office space, office furniture, phone systems, and clerical staffing as well as mentoring, access to capital, and other assistance to those companies who are accepted. They also play a large role in assisting a business with getting funding. Incubators are responsible for assisting in the start of thousands of companies each year. Their objective is to accelerate the time it takes to get a company’s products or services to market, many times in less than 6 months, and often in no more than 90 days. And of course, make the incubator a tidy profit. Venture capital companies, entrepreneurs, and corporations have founded private Incubators.

Incubators will charge a fee or more likely take some kind of equity in the business for their services. The great thing though is incubators are very selective. As you would imagine they receive way more applications then they can take, but if you get accepted you are in an elite group. That selection process is what puts you in an environment with many great companies and ideas.

An advantage of the incubator is that often member companies can take advantage of professionals, such as attorneys, accounting firms, marketing firms and others who are willing to either provide their services at a discount rate or, more likely, for an equity share.

Every incubator has an application process and usually deadlines for how many they will take in a given period. So you need to be on top of your game to get in and meet all the deadlines.

Should one join an incubator or a startup accelerator?

The main difference between an incubator and accelerator is that an accelerator is usually more time-sensitive, sort of like a “startup boot camp” for a few months to help you figure out whether your company has legs or if you should “fail fast” and move onto the next opportunity.

What you get from an incubator are:

- An ecosystem of entrepreneurs

- Mentorship

- Experienced leaders to guide your business

- A head start to fundraising

The decision?

It’s personal. If you’ve sold a few companies, you may feel that an incubator/ accelerator is not for you. At the same time, the constant mentorship, connection making across industries, and co-working with like-minded entrepreneurs who are willing to stop and give you a hand, make it hard not to want it.

If you are new to entrepreneurship, there’s definitely no looking back. Quoting the words of Steve Jobs, “Stay Hungry, Stay Foolish”, there’s never a better time than now to start your business; just do it smart.

Related articles

Contact us

Leave us basic information about a project and we will get back to you with answer

Need instant answers?

Our AI assistant is available 24/7 to answer questions on pricing, timelines, and project scope.

Click Here